Why We Stick To The Revolution Investing Playbook

There isn't one right way to invest. As we might say in rural New Mexico, "There are more ways than one to skin a cat." Warren Buffett, George Soros, Jim Simons, Peter Lynch, and Paul Tudor Jones radically diverged in their approaches to investing, and all of them were successful. Many others have attempted to replicate the success of the greats to no avail. That's why we have to pave our own way, while also attempting to learn as much as we can from those that came before. Regardless of the investing method employed, discipline, flexibility, conviction, hard work, and a little luck are universally required ingredients for a successful investing career.

The Revolution Investing approach we've refined over the last 20 years or so is unique to us and it's been successful (knock on wood). While we are constantly refining how we do what we do, our main job is to stick to the playbook that's worked so well for us over the last two decades. In this article, we wanted to lay out why we invest the way we do, and compare that to some of the other common investment strategies in our space. This isn't an exercise in self-aggrandizement, it's simply us codifying what we do.

Cody's style of investing, what we often call "Revolution Investing" is unique in the marketplace. If we could sum up our investment process, it would go something like this:

We invest in the companies building the most Revolutionary technology on the planet with highly differentiated business models and tremendous growth opportunities, while also paying extraordinary attention to valuations, economic cycles, and the trends in the broader markets in order to protect against downside risk.

Right now, most investors face this dilemma:

- Option 1: Chase disruptive tech or "innovation" with little valuation discipline or cycle awareness → huge drawdowns.

- Option 2: Hide in passive indexes → never beat the benchmark.

- Option 3: Avoid tech altogether → miss the most important wealth-creating trends of our lifetimes.

Our style really sits somewhere between Option 1 and Option 2. Most investors face a false choice between avoiding Revolutionary technologies, chasing them speculatively, or passively owning the market. Our process bridges that gap: we build core positions in proven leaders, actively manage around cycles and valuations, and selectively add exposure to the next generation of companies with true 10x–100x (or more!) potential.

So what makes our style different? When considering our Revolution Investing strategy at first glance, it might sound sort of like "thematic" investing. Google defines thematic investing as "an investment strategy that focuses on identifying long-term, macro-level trends and investing in companies that stand to benefit from them." This is basically the Cathy Wood approach. She identifies big trends that she is excited about – AI, energy storage, genomics, etc. – and then buys a bunch of companies that are playing in that trend.

The problem with a purely thematic approach is that it focuses more on the theme than the individual companies, and in our opinion often leads to the ownership of low-quality companies that are just riding the hype surrounding the theme. The themes that Cathy is following, like AI, are often the right themes, but then she ends up owning low-quality businesses like Teladoc Health (TDOC), 2U (TWOU), Pacific Bioscience (PACB), and others. For every good company in a theme – like Tesla (TSLA) for AI/Robotics – there are a hundred imitators, pretenders, and outright scams.

Under our approach, we employ a very high level of due diligence to ensure that the companies that say they are Revolutionary are actually Revolutionary. Moreover, we ensure they have the management prowess and balance sheet to execute on their Revolutionary vision. Here is the basic framework for how we evaluate individual companies:

Step 1: Know the Vision

- From the outset, we have to know the company’s Vision and the potential of what it could be in the long run.

Step 2: Monitor the Execution

- We require demonstrable execution on the Vision within a fixed amount of time (this is company specific of course).

- Our key performance indicators may include (1) major improvements in successive iterations of the company’s products/services (e.g. Moore’s-Law-type curves); (2) achieving targeted/modeled revenue growth; (3) improving profitability; (4) achieving scale in manufacturing; (5) rapid customer adoption; (6) ensure adequate balance sheet to achieve scale.

Step 3: Evaluate Management

- How much faith do we have that management can do what they say (or we think) they can do?

- Look at their history (e.g. Elon’s history of repeatedly achieving the impossible).

- Always “Bet on Brilliance.”

Step 4: Trust Our Analysis!

Think about the Robotics Revolution for example. People have been dreaming about autonomous humanoid robots since the 1800s, but no one has successfully produced them at scale yet. That's because this is an incredibly hard problem to solve, takes years of R&D, requires the most advanced AI in existence, and incredible manufacturing capabilities (and capital) to scale. There is really only one company today that has a reasonable chance of pulling this off (Tesla), and the next most likely competitors would be the companies building the AI platforms to power robotics like Nvidia and Google. We also have confidence in Elon's ability to achieve the impossible (he's done it a half dozen times already), and Tesla has the capital and manufacturing capabilities to do this at scale.

And while we do make speculative bets from time to time, the bar for a venture-style company to make it into the portfolio is extremely high (they have to make it through the same framework above). Moreover, we never chase hyped up theme/meme stocks just because they happen to be in a sector we are interested in.

Essentially, our avoidance of overvalued, hyped-up, or scammy companies is one of the primary ways we manage risk. In the long run, we know that the stocks of good companies with growing earnings will perform well, so we aren't really worried about short-term draw downs (we usually buy more!). And while we aren't going to nail every top, by avoiding the sh** companies, we can protect the against massive, permanent drawdowns. Remember, the ARK Innovation Fund (ARKK) is still down 50% from its all time high while the QQQ is up about 73% since then:

On the other end of the spectrum, traditional "value" investors obsess over near-term valuation metrics like EV/EBITDA, price/book value, FCF yield, etc. However, these metrics cannot account for the growth potential present in Revolutionary companies. This nearsightedness leads most value investors to miss out on some of the most incredible opportunities in the market. As Cody often says, all investing is "value" investing (no one consciously seeks to pay more than their estimation of a company's fair value). But many value investors don't have the vision to see how a company that looks expensive on paper today can actually grow revenue and earnings over the long term, in which case it might look quite cheap on a five, or ten year basis.

To arrive at a sense of fair value, we build financial models for every company we own looking out five, ten, and even fifteen years. Typically, we'd like to see a company have a five-year price/profits ratio in the single digits, and when we put a future multiple on those earnings, we are looking for an annualized return of 20%+. Of course, some of the most speculative bets require us to look out even further, and in those instances we have to size the position appropriately to account for the additional risk.

Like so many other things in investing, determining whether a company is fairly valued or not is an art, not a science. Every company is different, and the valuation they command depends on their unique positioning in the market. But our models help us visualize how a company succeed, and if they do succeed, whether we will earn an adequate return on our investment based on the current purchase price. Our models may end up being wrong, but they keep us grounded and at a minimum keep us from wildly overpaying for a company.

The difficulty of investing in Revolutionary tech without overpaying for growth has left a lot of investors choosing a third option: index investing. Index investing seems to offer the best of both worlds. American tech companies dominate the indices, and a lot of people are content to ride the indices as they've performed quite well on the backs of the dominance of American tech. So they get exposure to growing tech trends while avoiding the most speculative corners of the market.

This approach is fine for a lot of people, but it lacks exposure to some of the undiscovered, Revolutionary tech names that are not appropriately represented in the indices. Moreover, index investing fails to capture a lot of the value that we can capture when we get big dislocations in the megacap tech names that we see from time to time. This is where our approach active management can help drive superior returns. We are constantly assessing our positions against the market and "trimming" and "nibbling" as the opportunities present themselves.

Moreover, when the dislocations get extreme, we take the opportunity to load up on our favorite names, making high-conviction, concentrated bets on the biggest and best companies when their stock prices are getting punished by the market. You would think that as large and dominant as these companies are, the market would never sell them off, but it's amazing how often these megacap tech names get beat up and crash for one reason or another.

Think of our Google trade earlier this year for example. We were pounding the table on Google when the stock was around $160 in May of this year. At that time, the stock was down around 23% from its recent highs, and was significantly underperforming the indices as everyone was worried about the AI threat to Google's search business. We've owned Google for a very long time (Cody bought it on the day of the IPO), know the business extremely well, and when we did our homework, we were more confident than ever in Google's AI strategy. We saw an opportunity to load up on one of our favorite names at a cheap valuation (about 15 forward p/e, five-year p/p of 7) that is also at the forefront of building out the Revolution we are most excited about at present (AI). We made Google our second largest position at that moment, and it was our largest position when we included the exposure we had in call options on the stock.

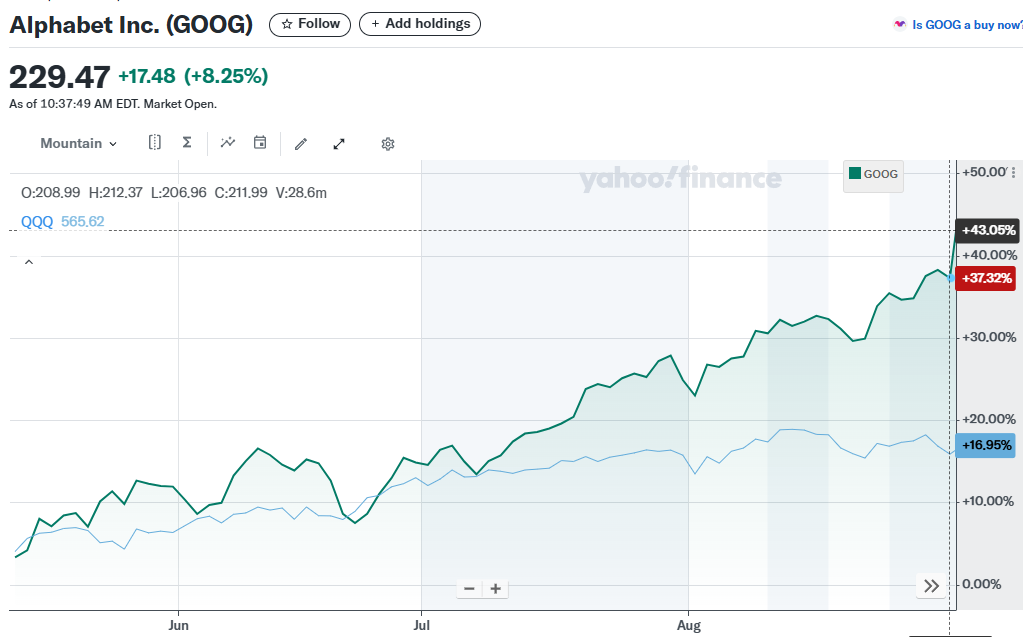

Today, Google put in a new all time high (the stock is currently at $230, up about 8.6% today) after the Federal judge overseeing the antitrust trial ruled that Google didn't have to sell its Chrome browser or divest the Android operating system. We've sold all the calls we owned, but Google is still our second largest position and we continue to think this is a stock that has a lot of room to grow over the next ten years or so as the company is one of, if not the leading AI company.

The point of the Google story is that there is a lot of opportunity to outperform the markets by actively managing our megacap exposure. Google is up about 43% since the date of our Deep Dive, compared to just 17% for the Nasdaq 100 ETF (QQQ):

Of course, we are not perfect and we have made mistakes (and unfortunately will occasionally still make mistakes) – but acknowledging those mistakes and fixing them is part of the process. But over time, we are confident that our approach to Revolution Investing will deliver outperformance compared to the indices, the average tech/innovation funds, and the old-school value funds. We might not catch every 10- or 100-bagger in the short run, but we also expect that we won't own the overhyped stocks that end up crashing 90%+ from their highs and never recover.

At the end of the day, investing is an art, not a science. We've developed a system that works for us, and our main job now is to believe and trust in that system over the long term.

That's it for now. Also, we'll do the Live Q&A Chat today at 12:00pm ET in the Discord Channel or you can email your questions to support@tradingwithcody.com.